Appearance

Insurance Risk Radar

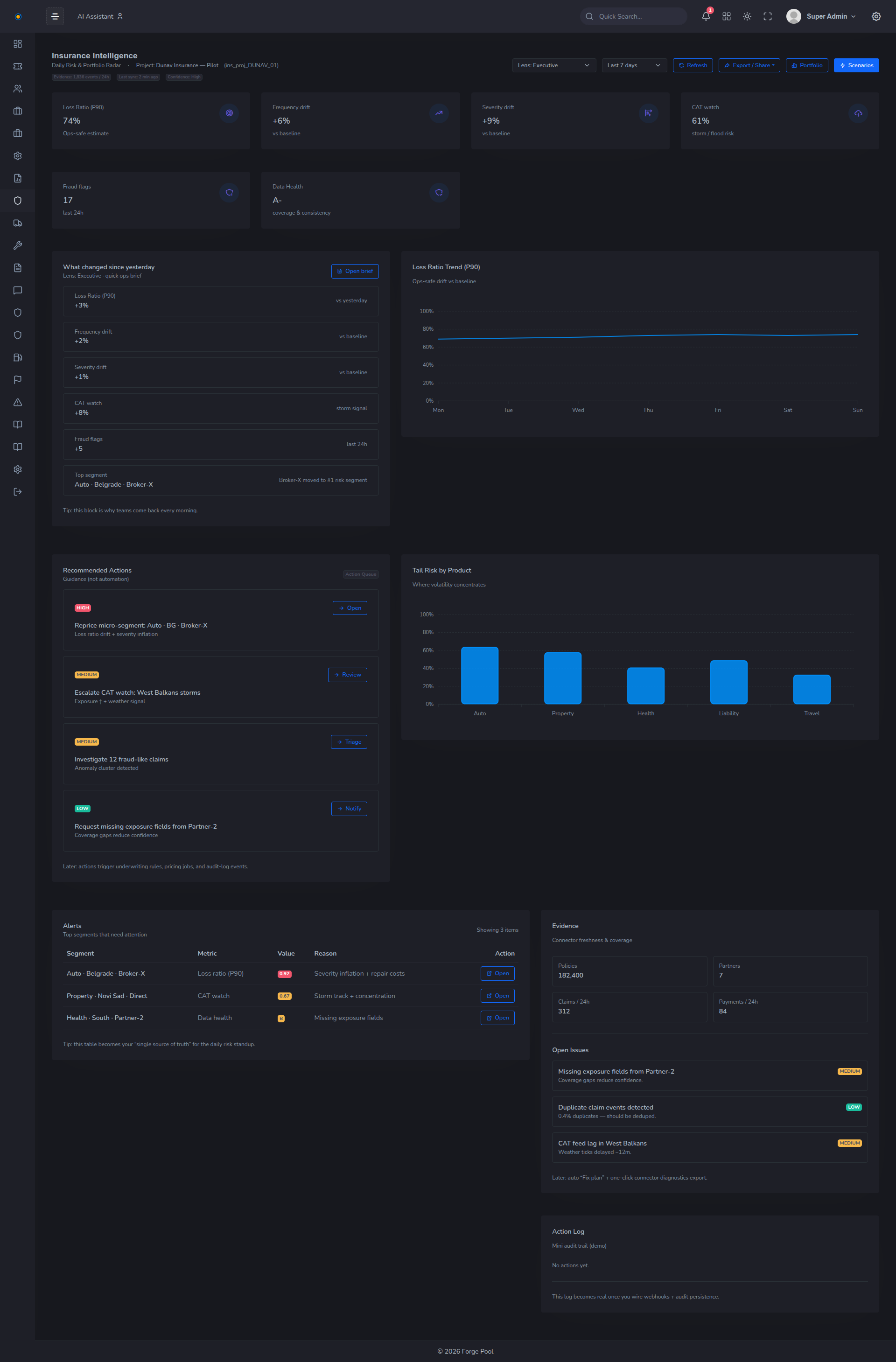

The Insurance Risk Radar is a live control room for portfolio-level risk visibility.

It aggregates probabilistic signals across policies, products, regions, and time horizons — allowing insurers to observe risk drift before it materializes into losses.

What Runs Here

This lab executes:

- probabilistic loss simulations

- CAT exposure aggregation

- severity and frequency drift analysis

- data health and coverage diagnostics

Execution is continuous and state-aware.

What Decisions It Supports

Operators use the Risk Radar to:

- detect early portfolio stress

- identify concentration risk

- adjust underwriting or pricing posture

- escalate CAT or systemic signals

Actions are guidance-driven, not automated.

Why It Is Trustworthy

Every signal shown is backed by:

- deterministic execution seeds

- replayable simulation runs

- traceable data inputs

- auditable artifacts

The radar shows not just what changed, but why it changed.

→ Related Solution: Insurance Intelligence

→ Related Adapter: Risk, Monte Carlo, CAT